News

better business decisions

Posted 18 hours ago | 4 minute read

Rethinking P415

The recent wave of modification proposals P509, P510 and P511 has prompted renewed attention on P415 and its role in enabling flexibility in Great Britain’s wholesale electricity market. With all three now awaiting an Urgency decision from Ofgem. In this article we look at what P415 was designed to achieve, how it is currently being used, and what these proposed changes might mean in practice.

What changed with P415?

In October 2023 Ofgem issued its decision on BSC Modification P415, titled “Facilitating Access to Wholesale Electricity Markets for Flexibility Dispatched by Virtual Lead Partners (VLPs)”. The modification was implemented on 7 November 2024, marking a watershed moment for the UK’s electricity market.

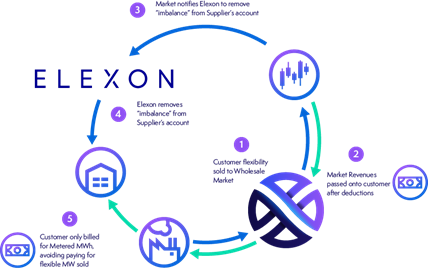

In essence, the modification enables independent aggregators to access wholesale markets without the need for a supply license. Flexibility from traditional demand response, distributed energy resources (DERs), electric vehicle (EV) charging hubs, and other behind-the-meter assets can now be sold into the wholesale market through these aggregators.

Virtual Lead Parties (VLPs) are aggregators that work on behalf of electricity generators and consumers to offer balancing services for the electricity system. In the previous arrangement, only suppliers could take physical actions in the wholesale market, with VLPs dependant on Trading Parties (typically an energy supplier) to participate in the wholesale market. This means that VLPs had limited ability to compete in the market with the only accessible markets being ancillary services, Capacity Market and the Balancing Mechanism.

The P415 change effectively delinks the wholesale trading role from a supply license, which can be quite costly to acquire. Independent aggregators and VLPs, are now able to trade in the wholesale market on the same terms as other Trading Parties, opening up new business models and sources of revenue for market participants.

P415 represented a significant step in opening up flexibility beyond the traditional supplier model. This matters because broadening participation in flexibility is essential to managing the transition to Net Zero at least cost. But P415 was not designed without constraints.

Under the current framework, participants are only rewarded for reducing demand, not increasing it. The impact on the host supplier is compensated through a mutualised mechanism, meaning the costs are spread across all consumers. The original impact assessment concluded that these costs would be outweighed by the benefits of increased flexibility participation and reduced peak prices. But there are concerns that some generators are using P415 arrangements to increase their revenues, drawing on the mutualisation fund without delivering the intended system benefits. If borne out, this would undermine the original economic case for the modification by increasing costs without a corresponding reduction in peak demand or prices.

Each of the new modification proposals seeks to address this issue, but they do so in quite different ways.

Proposed modifications

- P509 (Consumer benefits and safety net for Demand Side Response participation in the wholesale market) proposes a framework to assess whether individual participants are delivering outcomes consistent with the original impact assessment, and to take action where they are not. The challenge lies in the complexity of applying a baseline at the level of individual participants. Such an approach risks being difficult to administer and open to dispute.

- P510 (Introducing Direct Compensation for Virtual Trading Party actions in the Wholesale Market) represents a more fundamental redesign. It introduces a direct compensation mechanism, requiring the flexibility provider to pay the host supplier for the impact of demand changes, thereby removing the need for mutualisation. It also expands the scope of P415 to include both increases and reductions in demand.

- P511 (Removing Large-Scale Generation Assets from P415 Wholesale Market Activation Notifications) takes a direct approach by excluding generators above a defined threshold from participating in P415. This targets the perceived source of unintended behaviour without fundamentally altering the design of the mechanism. As a result, it is widely seen as a pragmatic and low-risk intervention that could be implemented on an urgent basis.

These proposals highlight the tension between preserving the benefits of an innovative mechanism and addressing emerging risks in its implementation. Targeted interventions such as P511 may offer a proportionate response to specific issues, while broader reforms like P510 require more detailed scrutiny to ensure they deliver on their objectives.

The central question should remain how best to support a growing flexibility market that delivers genuine value to consumers. Ensuring that incentives remain aligned with system needs, and that costs are justified by measurable benefits, will be key to maintaining confidence in the framework as the energy system continues to evolve.

Latest energy insights

-

Press Release

Press Release

26 March 2026

3 minute read

GridBeyond and Optima Energy sign agreement to help customers unlocking new revenues

Read More -

26 March 2026

4 minute read

How AI is helping data centres lead the next wave of grid flexibility

Read More -

Brochure

Brochure

24 March 2026

1 minute read

Whitepaper| USA | Risk transfer solutions in merchant energy markets | Downside protection strategies for battery storage assets

Read More -

Press Release

Press Release

17 March 2026

3 minute read

Samsung Ventures joins GridBeyond’s shareholder base as part of a €12M equity investment

Read More